# 基于求解器的投资组合优化问题的二次规划

说明关于基本投资组合模型的基于求解器的二次规划的示例。

此示例说明如何使用 quadprog 中的内点二次规划算法来求解投资组合优化问题。函数 quadprog 属于 Optimization Toolbox。

在此示例中定义问题的矩阵是稠密矩阵;然而,quadprog 中的内点算法也可以利用问题矩阵的稀疏性来提高速度。

# 二次模型

假设存在

令

经典的均值-方差模型是在一组约束条件下最小化投资组合风险,风险可由下式衡量:

其中约束如下:

预期回报率不应低于投资者期望的最低投资组合回报率

, 投资组合比例

的总和应为 1, 而且作为比例(或百分比),它们应为介于 0 和 1 之间的数字,

由于最小化投资组合风险的目标函数是二次型的,而约束是线性的,因此该优化问题是二次规划,即 QP。

# 225 项资产问题

现在让我们求解包含 225 项资产的 QP。该数据集来自 OR-Library [Chang, T.-J., Meade, N., Beasley, J.E. and Sharaiha, Y.M., "Heuristics for cardinality constrained portfolio optimisation" Computers & Operations Research 27 (2000) 1271-1302]。

我们加载数据集,然后按 quadprog 所需的格式设置约束。在此数据集中,回报率

加载存储在 MAT 文件中的数据集。

using TyOptimization

using TyMath

using TyPlot

using TyBase

path = pkgdir(TyOptimization)

data = load(path * "/data/port5.mat")

基于相关矩阵计算协方差矩阵。

Covariance = Correlation .* (stdDev_return * stdDev_return');

nAssets = length(mean_return); r = 0.002; # number of assets and desired return

Aeq = ones(1,nAssets); beq = 1; # equality Aeq*x = beq

Aineq = -mean_return'; bineq = -r; # inequality Aineq*x <= bineq

lb = zeros(nAssets,1); ub = ones(nAssets,1); # bounds lb <= x <= ub

c = zeros(nAssets,1); # objective has no linear term; set it to zero

# 在 Quadprog 中选择内点算法

为了使用内点算法求解 QP,我们将选项算法设置为 'interior-point-convex'。

options = optimoptions(:quadprog,Algorithm = "interior-point-convex");

# 求解 225 项资产问题

我们现在设置一些额外的选项,并调用求解器 quadprog。

设置附加选项:打开迭代输出,并设置更严格的最优性终止容差。

options = optimoptions(options,Display = "iter");

调用求解器并测量挂钟时间。

@time x1,fval1 = quadprog(Covariance,vec(c),Aineq,[bineq],Aeq,[beq],vec(lb),vec(ub),[],options);

Iter Fval Primal Infeas Dual Infeas Complementarity

0 7.212813e+00 1.975147e+03 2.230265e-01 2.121324e+01

1 5.087187e-04 1.360917e+00 1.536699e-04 2.830551e+00

2 3.936395e-04 8.181869e-01 9.238672e-05 4.511132e+00

3 3.525742e-04 2.468966e-01 2.787868e-05 7.635321e-01

4 5.519330e-04 1.234483e-05 1.393936e-09 1.487781e+00

5 5.519320e-04 1.923520e-09 2.455588e-13 2.376074e-04

6 4.680051e-04 3.926649e-10 5.012570e-14 7.796372e-05

7 3.606961e-04 1.377623e-11 1.753372e-15 1.406325e-05

8 2.982304e-04 1.989739e-14 3.686287e-18 1.085233e-05

9 2.729816e-04 1.874721e-14 2.493665e-18 4.602483e-06

10 2.238534e-04 1.014434e-14 5.854692e-17 4.445010e-05

11 2.099378e-04 1.628271e-14 2.818926e-18 6.357395e-06

12 1.971963e-04 1.986036e-14 1.246832e-18 7.627446e-07

13 1.952795e-04 1.820585e-14 8.673617e-19 3.467287e-08

14 1.949127e-04 1.989459e-14 1.002887e-18 1.305679e-10

Minimum found that satisfies the constraints.

Optimization completed because the objective function is non-decreasing in feasible directions, to within the value of the optimality tolerance and constraints are satisfied to within the value of the constraint tolerance.

0.282460 seconds (5.12 k allocations: 64.743 MiB, 12.99% gc time)

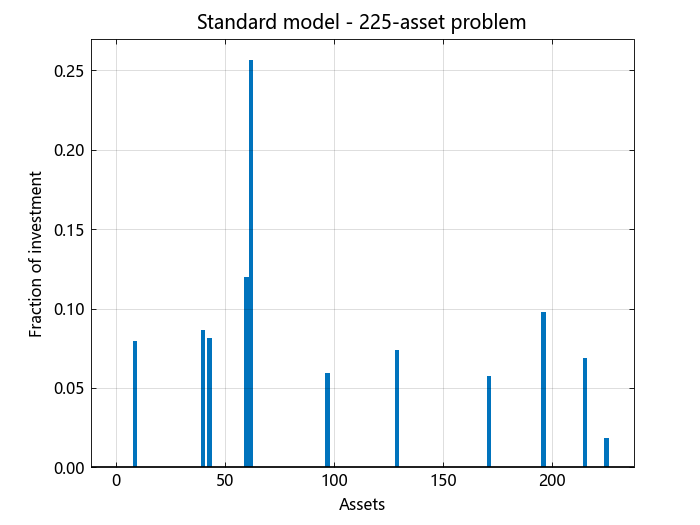

绘制结果。

bar(x1,width = 2)

ylabel("Fraction of investment")

xlabel("Assets")

title("Standard model - 225-asset problem")

grid("on")

# 具有组约束的 225 项资产问题

我们现在向模型增加一组约束,即要求投资者 30% 的资金必须投资于资产 1 至 75,30% 投资于资产 76 至 150,30% 投资于资产 151 至 225。每组资产可以是不同行业,例如技术、汽车和制药。

实现此新要求的约束为:

向现有等式约束添加这组不等式约束。

Groups = blkdiag(ones(1,div(nAssets,3)),ones(1,div(nAssets,3)),ones(1,div(nAssets,3)));

Aineq = [Aineq; -Groups]; # convert to <= constraint

bineq = [bineq; -0.3*ones(3,1)]; # by changing signs

调用求解器并测量挂钟时间。

@time x2,fval2 = quadprog(Covariance,vec(c),Aineq,vec(bineq),Aeq,[beq],vec(lb),vec(ub),[],options);

Iter Fval Primal Infeas Dual Infeas Complementarity

0 7.212813e+00 2.304305e+03 5.062751e+00 2.598079e+01

1 5.014626e-04 1.446136e+00 3.177280e-03 3.299995e+00

2 4.043363e-04 8.119089e-01 1.783832e-03 2.442291e+00

3 3.474328e-04 2.375218e-01 5.218552e-04 1.628265e+00

4 3.829175e-04 1.187609e-05 2.609276e-08 3.536073e-01

5 3.829158e-04 1.191021e-09 2.628376e-12 3.943413e-05

6 3.536513e-04 2.790679e-10 6.158524e-13 1.232625e-05

7 2.965677e-04 2.469723e-11 5.447932e-14 5.401752e-06

8 2.621091e-04 1.974690e-14 7.209944e-18 2.979064e-06

9 2.234785e-04 1.310451e-14 2.276825e-18 5.842570e-06

10 2.082052e-04 1.542020e-14 1.084202e-18 1.104407e-06

11 2.027746e-04 1.886318e-14 2.114194e-18 3.336141e-08

12 2.009830e-04 2.021292e-14 9.486769e-19 1.646531e-09

Minimum found that satisfies the constraints.

Optimization completed because the objective function is non-decreasing in feasible directions, to within the value of the optimality tolerance and constraints are satisfied to within the value of the constraint tolerance.

0.240488 seconds (5.03 k allocations: 62.282 MiB, 6.91% gc time)

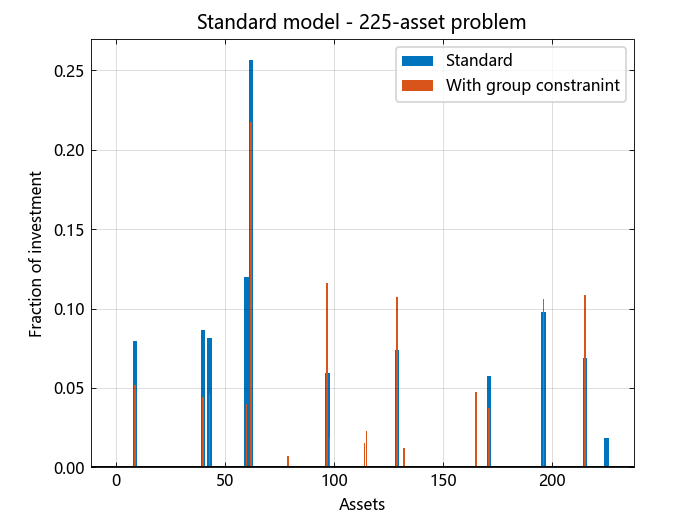

绘制结果,叠加在先前问题的结果上。

hold("on")

bar(x2)

legend(["Standard","With group constranint"])

hold("off")

# 迄今为止结果摘要

我们从第二个条形图中看到,由于存在额外的组约束,与第一个投资组合相比,现在投资组合在三个资产组中的分布更均匀。这种强加的多样化也导致风险略微增加,这是通过目标函数来测量的(请参阅两次运行的迭代输出中最后一次迭代的标记为“f(x)”的列)。

# 使用随机数据的 1000 项资产问题

为了说明 quadprog 的内点算法如何处理更大型的问题,我们将使用包含 1000 项资产的随机生成的数据集。

重置随机流以实现可再现性。

rng = MT19937ar(0);

nAssets = 1000; # desired number of assets

生成 -0.1 到 0.4 之间的回报率均值数据。

a = -0.1; b = 0.4;

mean_return = a .+ (b-a).*rand(rng,nAssets,1);

生成 0.08 到 0.6 之间的回报率标准差数据。

a = 0.08; b = 0.6;

stdDev_return = a .+ (b-a).*rand(rng,nAssets,1);

# Correlation matrix, generated using Correlation = gallery('randcorr',nAssets).

# (Generating a correlation matrix of this size takes a while, so we load

# a pre-generated one instead.)

path = pkgdir(TyOptimization)

data = load(path * "/data/correlationMatrixDemo.mat")

# Calculate covariance matrix from correlation matrix.

Covariance = Correlation .* (stdDev_return * stdDev_return');

# 定义并求解随机生成的 1000 项资产问题

我们现在定义标准的 QP 问题(此处没有组约束)并求解。

r = 0.15; # desired return

Aeq = ones(1,nAssets); beq = [1]; # equality Aeq*x = beq

Aineq = -mean_return'; bineq = [-r]; # inequality Aineq*x <= bineq

lb = zeros(nAssets); ub = ones(nAssets); # bounds lb <= x <= ub

c = zeros(nAssets); # objective has no linear term; set it to zero

@time x3, = quadprog(Covariance,c,Aineq,bineq,Aeq,beq,lb,ub,[],options);

Iter Fval Primal Infeas Dual Infeas Complementarity

0 2.144124e+01 1.306964e+04 2.686312e+00 4.519961e+01

1 9.603334e-02 1.156196e+02 2.376427e-02 5.507976e+00

2 9.472022e-05 9.980635e-01 2.051404e-04 9.096405e-02

3 7.912080e-05 4.990318e-05 1.025702e-08 1.035340e-03

4 7.905810e-05 2.067984e-08 4.250529e-12 1.123253e-06

5 3.353342e-05 2.173559e-10 4.471614e-14 4.747129e-07

6 1.856073e-05 6.550039e-14 1.111307e-17 4.743841e-07

7 1.458766e-05 8.263706e-14 2.289530e-18 2.539410e-08

8 1.371413e-05 8.318969e-14 9.911344e-19 9.405355e-10

Minimum found that satisfies the constraints.

Optimization completed because the objective function is non-decreasing in feasible directions, to within the value of the optimality tolerance and constraints are satisfied to within the value of the constraint tolerance.

2.605711 seconds (15.60 k allocations: 722.423 MiB, 2.48% gc time)